The economy rebounded during the second quarter, bolstered by larger consumer tax refunds and continued business investment in technology. However, the Iran conflict introduced new uncertainty, triggered an oil price shock, and renewed inflationary pressures. As a result, the benchmark 10-year Treasury yield rose to its highest level in more than a year during May. Against this backdrop, the Federal Reserve (the Fed) maintained its focus on inflation and left policy rates unchanged.

Residential Real Estate

Economic uncertainty contributed to a measured pace of activity in the residential housing market this spring. Improved affordability encouraged purchases during the quarter, as reflected by Existing and New sales that improved 2.0% and 5.3% over Q1, respectively. Builders facing elevated inventory levels raised their price concessions1 and sale incentives, while many existing homeowners reduced asking prices2 to attract buyers. The importance of location may have become even more pronounced, as illustrated in the latest FHFA House Price Index Quarterly Report.

Beyond pricing, buyers and sellers appeared increasingly willing to adapt to a market characterized by elevated interest rates and economic uncertainty. As Realtor.com noted, participants are developing a more “recalibrated attitude” toward these conditions. This change was evident in new listings in May that reached their highest level in four years, in addition to the jump in first-time home buyers3 willing to come off the sidelines. However, improving activity was constrained by weaker buyer confidence and the highest 30-year fixed mortgage interest rates in nine months. Builders also scaled back housing starts as they worked through elevated inventory levels and rising material costs.

Commercial Real Estate

The CRE market remained resilient during the second quarter, despite encountering several new headwinds. Investors and lenders remained active but cautious as they assessed the inflationary implications of the conflict in Iran and the mid-May surge in the benchmark 10-year treasury4 yield.

Transaction volume across the four major property sectors is projected to reach approximately $74 billion, slightly below last quarter, according to an analysis of CoStar data. Even so, annual growth remained in the double digits, while property prices continued to rise. Delinquencies edged higher in Q1 but remained uneven across property types and had limited impact on distressed transaction activity. Retail cap rates increased modestly, largely due to movement in the mall segment.

Property fundamentals continued to normalize across major asset classes, per CoStar. Office performance improved gradually, while limited new supply supported Retail occupancy. Multifamily fundamentals strengthened as construction starts fell to a decade low. Industrial continued to work through speculative inventory, with vacancy and rent growth returning to more typical levels. Despite transportation-related disruptions from the conflict in Iran, technology-driven manufacturing supported demand and absorption.

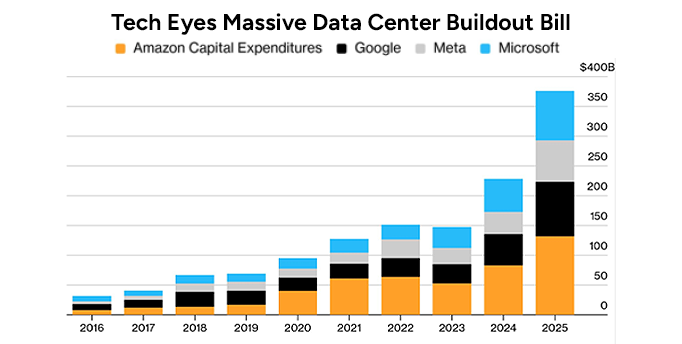

With the explosion of the Artificial Intelligence (AI) industry, data centers were a big driver of business investment, added construction employment, and supported the industrial manufacturing resurgence. Their inventory5 spans almost every region of the country. And although data center property and land sales were not a big portion of the overall CRE transaction pie, their growth was exceptionally strong.

In 2025, data center land transactions increased five-fold, while existing data centers’ sale volume rose 36%. Transaction activity through June for both types of sales was ahead of last year’s pace. Much of this activity was driven by the substantial expansion plans among major technology companies. However, the trajectory of future data center development is less clear. Although the federal government6 offers federal land for data centers, more states and localities7 are curbing or halting further expansion.

Source: Mortgage Bankers Association

A Glance Forward

The economy is expected to moderate during the second half of the year. Gross Domestic Product growth could dip below 2.0% again. Employment should be solid, although consumers face a fall in real wages while business investment normalizes. The MBA expects the oil price shock of the last few months to wind its way through inflation this summer, bringing no relief to the Treasury yield or mortgage rates. Although the Fed Funds rate was kept the same in Q2, Board members became more divided on the appropriate future path. Despite the new Fed Chair’s clear and often-stated commitment to the Fed’s 2% inflation target, no movement in the Fed Funds rate is expected at their July meeting (or even this year).

Existing and New home sales could receive more support from continued price adjustments and improved affordability. Median prices are expected to decrease and the FHFA House Price Index could drop below 1.0% for the first time in 14 years.

CRE transaction activity is expected to remain stable as property fundamentals continue to normalize. Indeed, if buyers and sellers are increasingly willing to bring prices together as recently reported8, it could provide additional momentum for transaction growth.

Sources:

1 National Association of Home Builders, “Builder Sentiment Remains Weak Amid Affordability Concerns.” June 15, 2026. Reprinted with permission July 2026. https://eyeonhousing.org/2026/06/builder-sentiment-remains-weak-amid-affordability-concerns/

2 Realtor.com, “May 2026 Monthly Housing Report: Sellers Are Meeting the Market—and Buyers Are Showing Up.” Reprinted with permission July 2026. https://www.realtor.com/research/may-2026-data/

3 Copyright ©2026 “May 2026 REALTORS Confidence Survey.” NATIONAL ASSOCIATION OF REALTORS®. All rights reserved. Reprinted with permission July 2026. https://www.nar.realtor/sites/default/files/2026-06/2026-05-realtors-confidence-index-06-09-2026.pdf

4 Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS10], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS10, July 2, 2026.

5 Avison Young, “U.S. data center update: Leasing and Capital Market trends Q1 2026.” Reprinted with permission July 2026. https://www.avisonyoung.us/documents/d/us/q1-2026-us-data-center-update?_gl=1*ejbwa2*_up*MQ..*_ga*MTgxMzY2NTU0MC4xNzgxNzIwOTU3*_ga_NB1T86YXFD*czE3ODE3MjA5NTYkbzEkZzEkdDE3ODE3MjEwMzAkajYwJGwwJGgw

6 Bisnow, “Biden Issues Executive Order Freeing Up Federal Land For Data Centers.” Reprinted with permission July 2026. https://www.bisnow.com/national/news/data-center/biden-issues-executive-order-freeing-up-federal-land-for-data-centers-powered-by-clean-energy-127558

7 Bisnow, “14 States, Dozens of Localities Consider Bans On Data Centers,” Reprinted with permission July 2026. https://www.bisnow.com/national/news/data-center-community-relations/14-states-dozens-localities-consider-data-center-bans-135009

8 Bisnow, “FIRST DRAFT LIVE: Have We Reached The End Of The Bid-Ask Standoff?” Reprinted with permission July 2026. https://www.bisnow.com/national/news/capital-markets/first-draft-live-have-we-reached-the-end-of-bid-ask-standoff-135183