Title Policy Remittances

Are title policy images and premium endorsement images uploaded directly into ezJacket in the Non-Remitted Policies screen prior to remitting?

Did you know that in StarsLink you can find helpful guides on how to process ORT Loan Modifications?

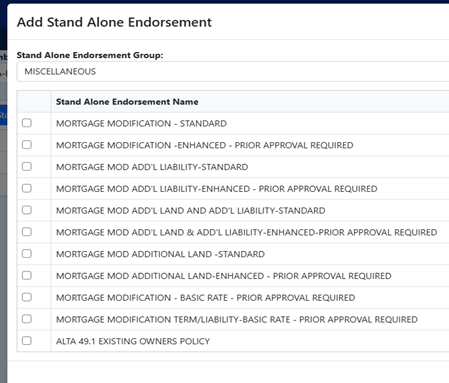

Do you know where the Mortgage Modification Endorsement fees are processed in ezJacket? These special endorsements are processed under the Create Miscellaneous screen to generate a Stand-Alone Endorsement fee.